EU VAT Rules for Digital Products and Services

Are you accounting for EU VAT and charging at the correct rate? If you accept online payments for digital products and services, these are the VAT rules you need to know.

Matt HagemannPublished September 4, 2019

The EU VAT rules we’re about to explain only apply to digital products and services. These are telecommunications, broadcasting and electronic services (TBE), or also called electronically supplied services (ESS) by the European Commission. They do not apply to physical goods, which have their own separate rules involving cross-border customs and taxes.

A digital product is any product that’s stored, delivered, and used in an electronic format. Your customer normally obtains them over the internet, by logging onto your website or via email after purchase.

If you want to learn more about TBE and whether your product potentially falls into that broad definition, we’ve written a more detailed guide about what digital products are.

Who Needs to Implement EU VAT rules

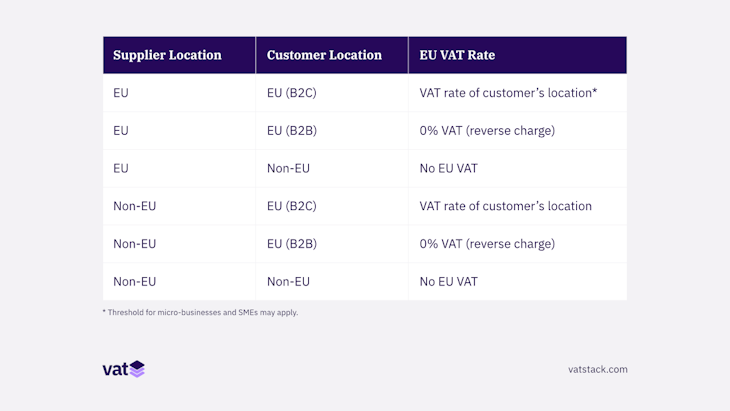

Every business that sells ESS to customers in the EU has to take EU VAT rules into consideration. To answer precisely what rules apply in your specific case, you need to know who the transacting parties are and where they are located at.

It’s practically a necessity to establish your customer’s country of residence (the place of supply) during a checkout process. One common method is to geolocate customers by their IP address.

Let’s start with the supplier’s side (you) since you will likely know more about yourself.

Supplies Within the Same Member State

Registration for VAT and charging VAT may be voluntary if revenues fall below certain thresholds. Please consult your local tax advisor to learn whether any thresholds apply.

If you’re a VAT-registered business selling to a customer in the same Member State, you normally charge the VAT valid in your home country.

You also charge VAT on digital products and remit the VAT with every quarterly reporting period. It is up to your customer to determine whether they are eligible to reclaim VAT that they had been charged. This is something to be dealt with between the customer and the tax administration, not with the supplier. Your obligation as a supplier is to provide a compliant VAT invoice, though.

It is common in the EU to always display prices inclusive of VAT. You may want to take this into consideration when pricing your products.

Example: A customer in the Netherlands signs up for hosting service from a company also located in the Netherlands. Since the VAT rate in the Netherlands is 21%, the subscription’s net price of 60 EUR per year is increased by 12.60 EUR. The customer, regardless of whether it’s a business or end-consumer, is charged 72.60 EUR a year and can use your invoice to reclaim VAT.

Intra-Community Supplies: EU Business Selling to Another Member State

If the transaction happens between two Member States, you have to mind differences in B2B and B2C. Member States come under the European Union VAT regime and are part of the EU single market economy.

VAT directives are issued by the EU which lay out the principles of the VAT regime to be adopted by the Member States. These directives take precedent over the local legislation.

In B2B, a reverse-charge mechanism applies whereby the obligation to account for VAT is reversed to the buyer. Since businesses generally don’t pay a VAT, the VAT on digital products is simply 0%.

To ensure, you’re actually dealing with a business, you need to let her input her unique VAT number, which you can validate with our validation API. A valid VAT number is currently a formal requirement for applying the zero VAT rate to intra-community supplies of goods.

Example: A business located in France subscribes to a SaaS operated by a startup in Germany. The French business enters their VAT number which the SaaS’ system immediately validates. As soon as it is confirmed valid, the monthly net price of 39 EUR remains unchanged (no VAT is applied). For each quarterly reporting period, the German startup should validate all their customers’ VAT numbers to ensure that they continue to be eligible for a 0% VAT. Use our bulk VAT number check tool, to re-validate your customers’ VAT numbers on a regular basis.

In B2C, things look a little differently. You charge VAT to all end-consumers. But the VAT rate depends on the size of your business and on where the consumer is located. In January 2019, a new threshold to ease the regulatory tax burden of micro-businesses and SMEs came into effect:

- If your annual turnover for digital products sold in the EU is below 10,000 EUR, you can charge the VAT rate of your home country.

- Once you pass the 10,000 EUR threshold, you must charge the VAT rate of the consumer’s country.

You can refer to the European Commission’s current and historical VAT rates for every Member State. We keep our VAT rates up-to-date and constantly track changes to legislations and recommend feeding your application or payment provider with the latest VAT rates.

Example 1: An Italian consumer buys an ebook with an ISBN priced at 10 EUR from a renowned marketplace operating in Ireland. Upon checkout, a chance to enter a VAT number is presented to the Italian consumer, but because she is not a business owner, she does not enter one. The standard VAT rate in Italy is 22%, but Italy has a reduced VAT rate of only 4% for ebooks that carry an ISBN. The final price is therefore going to be 10.40 EUR (including 4% VAT).

Example 2: A Belgian consumer signs up for an online course costing 500 EUR offered by a coach in Malta. The course materials are delivered to the consumer automatically via online downloads and no one-on-one sessions are provided. This renders the course fully automated and it falls under the digital product category. Since the coach has just launched the course, annual turnover is still below 10,000 EUR. She opts to benefit from the new VAT rules for micro-businesses and charges 18% VAT to all consumers across the EU. The final price for the Belgian consumer is 590 EUR (a competitive edge compared to the Belgian VAT rate of 21%).

Supplies by Non-EU Businesses: Selling From Outside the EU

Businesses not situated in the EU have it slightly easier in terms of determining what VAT rate to charge.

In B2B you should reverse-charge VAT, meaning that you don’t charge a VAT as long as a valid VAT number is presented by the customer. This means that you should implement some kind of real-time VAT number validation procedure into the checkout process. You also have to ensure that all customer VAT numbers are still valid with each quarterly reporting period for VAT remittance.

In B2C transactions, you always charge the VAT of the customer’s country. The European Commission publishes current and historical VAT rates for each Member State.

It’s worth highlighting that the non-EU supplier’s obligation to file VAT returns and pay VAT due arises with the very first Euro on sales of digital products in the EU consumer market. Unfortunately, there are no exceptions to these VAT obligations, no de minimis thresholds for turnover or transaction volumes.

We’ll guide you through a few tax treatment configurations when you sign up, so you know the most relevant rules and can be VAT-compliant from the get-go.

How to Remit VAT Collected From Customers

Mind that the concept of VAT is not to tax you as a business, but to tax your customer. VAT is a consumption tax specifically for the end-consumer. You can see yourself as the middleman that collects VAT on behalf of the various tax administrations. VAT is generally zero-sum for businesses, so you don’t have any monetary disadvantage other than the efforts for implementation and compliance.

You’ve now been collecting VAT from your customers and the amounts are piling up. Here are the basics:

Within 10 days of the first sale of a digital product to an EU customer, you must register with the tax administration of the Member State where your customer resides. There are 28 countries in the EU (27 after Brexit, but that doesn’t help) and if you have customers across the EU, this quickly becomes a bureaucratic nightmare.

The EU has therefore introduced a so-called One-Stop Shop (OSS) scheme on July 1, 2021. This scheme lets suppliers file quarterly VAT returns to a single tax administration of their choice and that tax administration will do the distribution of funds to each Member State. There are two types of schemes:

- Union OSS for businesses based in the EU: You register for VAT to obtain a unique VAT number. Mind potential threshold allowances in your Member State before registering. You can then activate that VAT number for OSS.

- Non-Union OSS for businesses based outside the EU: You register for VAT with a tax administration of your choice. English speakers generally prefer to register for OSS with the UK or Ireland. Since Brexit, the safer option is Ireland.

You then use their platforms to perform VAT reporting and remittance on a quarterly basis. Deadlines for filing VAT OSS returns are found in a dedicated article.

Evidence for the Place of Supply

You must collect two pieces of evidence that confirm your customer’s location and keep them on file for 10 years. This evidence could be:

- the billing address of the customer (valid only if provided by a 3rd party)

- location of the customer’s bank

- country of credit card issuance

- the Internet Protocol (IP) address of the device used by the customer or any method of geolocation

- country of the SIM card (in cases where the purchase was made on a mobile device)

- the location of the customer’s fixed land line through which the service is supplied to him

- other commercially relevant information (e.g. product coding information which electronically links the sale to a particular jurisdiction)

If you’re a business in the EU with less than 100,000 EUR in cross-border sales of ESS annually, then you only need to collect one piece of customer location evidence.

All evidence must be gathered from a third party, such as the bank or IP address, and not from the customer directly. After all, the customer could twist the facts to evade paying tax.

Use our API to store pieces of evidence for every transaction and have them ready whenever needed. We also store them automatically for you if you connect Vatstack with a payment provider like Stripe.

Evidence for a Reverse Charge

If you have a business or corporate customer, the VAT will be zero-rated. As mentioned above, this mechanism is called reverse charging. You need to

- show evidence that a customer has actively communicated the VAT number to you (it is not enough to search for the customer’s VAT number on the internet),

- state the VAT number on the customer invoice to legitimize zero-rating and

- file a European Commission Sales List (ESL) for zero-rated sales.

To check VAT numbers manually, use the VAT Information Exchange Service (VIES) of the European Commission. You can search and validate one VAT number at a time.

The VIES portal may experience scheduled maintenance and downtime periods on a regular basis and you would not be able to validate a VAT number during that period. Just try again at another time.

You can use our validations API to automate VAT number checks during checkout. All records are stored securely in the cloud for reporting purposes and contain a unique consultation number. A consultation number is a piece of evidence given by VIES to prove that you have validated a given VAT number on a given day.

How Vatstack Automates All VAT Rules

When you’re working on a checkout process, you can keep your VAT rates updated by pulling the rates from our API endpoint.

After that, generate price quotations whenever your customer is about to check out. Price quotation requests run through our tax engine to calculate the total price and the VAT due for every sale. It works seamlessly via API and takes regional settings you had configured in your dashboard to match it against your customer.

This means that all VAT rules explained above are centralized in the quotes API endpoint. The API’s response contains all the information you need to charge the correct price.